AMC Entertainment Holdings is not worth owning at any price, barring a drastic change to its business model. Given poor fundamentals and a mountain of debt (221% of market cap), we don’t see how equity investors will have a claim to any future profits, especially given the headwinds facing the movie theater industry.

Making matters worse, the company

AMC,

-5.32%

continues to issue new shares, like the recent 43-million share sale, so equity investors claims on any future profits are further diluted.

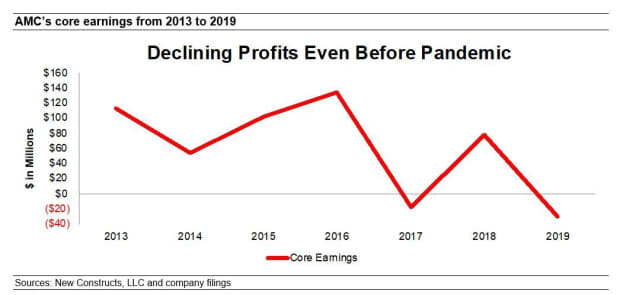

Fundamentals were bad before the COVID-19 pandemic

Movie theater operator AMC Entertainment had its moment as a meme stock at the same time it was staving off bankruptcy, which illustrates how little the stock’s rise was related to the firm’s fundamentals.

Apart from bankruptcy concerns, AMC’s business operations had been trending in the wrong direction even prior to the COVID-19 pandemic. We calculate that AMC’s core earnings fell from $114 million in 2013 to around $30 million in 2019. The firm burned through $5.2 billion in free cash flow (FCF) from 2014-2019. FCF was -$3.9 billion in 2020.

Given the poor fundamentals, AMC had earned our “unattractive” rating even before the meme-stock frenzy took off.

Pandemic headwinds persist

The shift away from movie theaters to streaming could be permanent. When COVID-19 shut down movie theaters across the globe, production studios initially postponed movie releases. As lockdowns persisted, movie studios started releasing their movies on streaming platforms such as Disney+ and HBO Max, often on the same day as in theaters. Gone was the exclusive window of about three months for theaters to cash in on new releases before they hit streaming platforms.

Now that consumers got a taste of new movie releases at home, there may be no return to the old model. In a survey conducted in May 2020, 70% of respondents indicated they would rather watch new movies at home, even if theaters were opened.

Accordingly, Disney

DIS,

-0.68%

began sending movies originally intended for theatrical release directly to its streaming service in mid 2020. Similarly, AT&T’s

T,

+0.62%

Warner Bros. announced in December 2020 that it would launch every 2021 movie on HBO Max at the same time as theaters. As David Sims, a writer for The Atlantic put it, “audiences will have little incentive to pay more to see these films in theaters.”

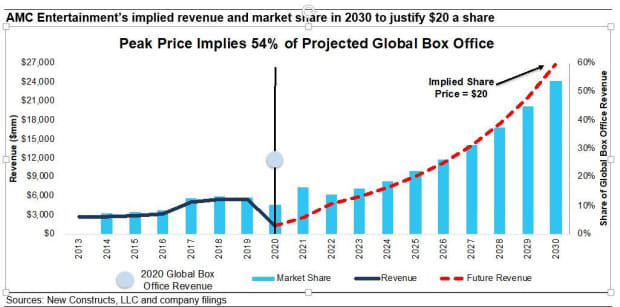

However, poor fundamentals and structural headwinds didn’t stop AMC Entertainment’s stock from soaring during the meme-stock frenzy. To give readers a sense of just how crazy-overvalued the stock was at its peak, we do the math and show how the business would have to perform to justify a price of $20 a share, which it reached in late January.

‘Crazy’ at $20 explained: It implies market share rises from 13% to 54%

Our reverse discounted cash flow (DCF) model shows that to justify a $20 share price, AMC Entertainment must:

- immediately improve its profit margin to 14%, which equals the highest in company history (2013), compared with 8% in 2019, and

- grow revenue by 36% compounded annually for the next decade, which is based on growing at consensus estimates in 2021 (113%) and 2022 (81%), and 24% each year thereafter (well above 9% consensus revenue estimate for 2023)

In this scenario, AMC Entertainment earns nearly $27 billion in revenue in 2030, which is nearly five times more than its previous record revenue of $5.5 billion in 2019 and around 220% of 2020 global box-office revenue.

If we assume global box-office revenue grows at projected rates from 2020 to 2025 and grows 3.7% a year (equal to CAGR from 2009 to 2019) from 2025 through 2030, the scenario above implies AMC Entertainment’s revenue would reach 54% of the global box-office revenue in 2030, up a good bit from about 13% in 2019.

This chart compares AMC Entertainment’s historical revenue and share of the global box office to its implied revenue and share of the 2030 projected global box office for this scenario.

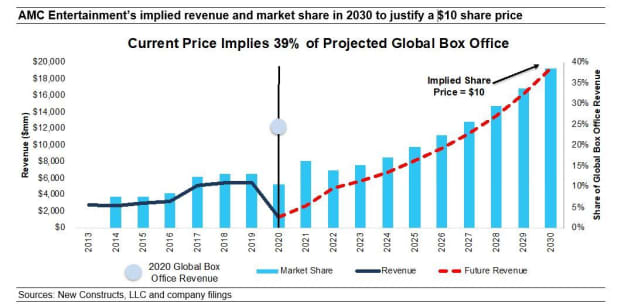

Still crazy at $10

For perspective on the current price, we run the same analysis to show what the company must do to justify a share price of $10 – which is lower than where it now trades:

- immediately improve its profit margin to 14% (its all-time high in 2013) and

- grow revenue by 32% compounded annually for the next decade (which is well above projected box office revenue CAGR of 21% through 2025) revenue.

In this scenario, AMC Entertainment’s revenue would be 39% of the estimated global box office revenue in 2030 (based on same assumptions as above). This next chart compares AMC Entertainment’s historical revenue and share of the global box office to its implied revenue and share of the 2030 projected global box office for this scenario.

The stock is not worth $1

Given that the performance required to justify a $10 share price is ridiculous, we dig deeper to see if this stock is worth buying at any price.

The answer is no.

Given $9.8 billion in total debt, $44 million in underfunded pensions, $40 million in net deferred tax liabilities and $27 million in minority interests, it is unlikely that the company will ever make enough money to satisfy stakeholders who have higher claims on the firm’s cash flows.

In other words, we do not think equity investors will ever see $1 of economic earnings.

AMC is selling stock to exploit gambling investors

Taking advantage of its ultra-high valuation, AMC sold around 312 million new shares in the fourth quarter of 2020 and the first quarter of 2021, or more than double the number of shares outstanding at the end of the third quarter of 2020, and significantly diluted investors’ equity stakes.

On Tuesday, it said it would sell another 43 million shares but called off its controversial plan to seek approval to issue 500 million shares.

Given the stock’s drop of more than 5% on Wednesday in a flat market, equity investors appear to be catching on that the company is cashing in on their gullibility by selling them shares at elevated prices.

Sure, raising cash staves off bankruptcy, but that delay only helps equity investors if the company can generate profits large enough to pay off debtholders and other stakeholders with senior claims. Even so, the likelihood of the company ever generating the future cash flows required to justify the current valuation is very, very low.

Buyer beware.

David Trainer is the CEO of New Constructs, an independent equity research firm that uses machine learning and natural language processing to parse corporate filings and model economic earnings. Kyle Guske II and Matt Shuler are investment analysts at New Constructs. They receive no compensation to write about any specific stock, style or theme. New Constructs doesn’t perform any investment-banking functions and doesn’t operate a trading desk. This is adapted from a report entitled “Saving Investors from Meme Stocks: AMC Entertainment.” Follow them on Twitter@NewConstructs.