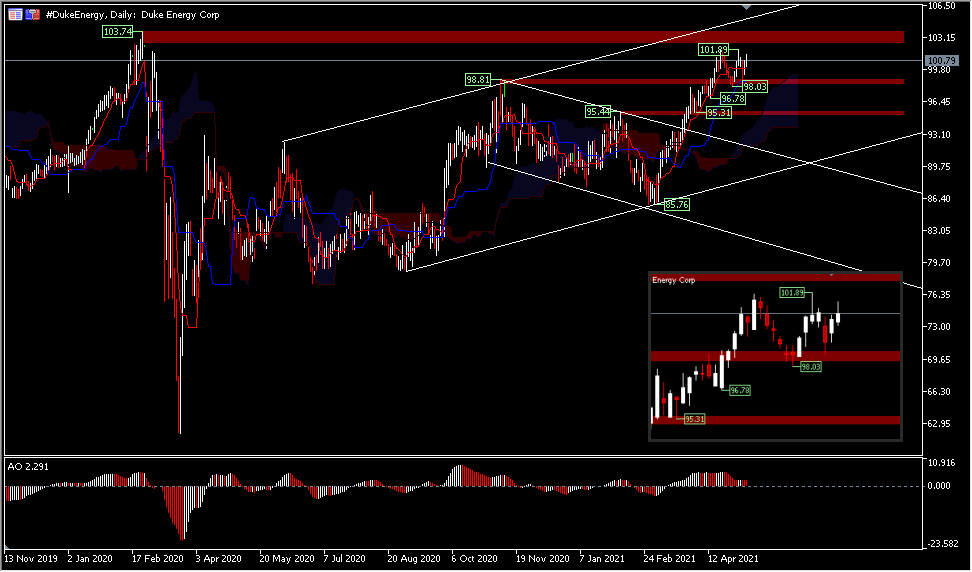

Duke Energy’s share price closed the week on Friday with a slight gain of +0.42% at $100.79. The performance, although quite positive, is still below the performance of May 3 which recorded a peak price of $101.89. The stock showed mixed performance when compared to some of its competitors on Friday, such as NextEra Energy Inc. NEE, which rose +0.70% to $74.53, Dominion Energy Inc. D, which weakened -0.04% to $78.45 and Southern Co. SO, which rose +0.32% to $66.26. Technically, Duke Energy still has the opportunity to strengthen, but ahead of the quarterly earnings report investors seem to be quite cautious. The historic high was at $103.74, in February last year.

Price bias is still showing on the positive side, although the momentum is starting to fade from the short AO histogram to the neutral side, however the average price movement is still above Kumo and above resistance which is now support at $98.81. A move above $101.89 could target the historic peak of $103.74. On the downside, if the price does not continue the rally it could target the $98.03, $96.78 and $95.31 support levels.

The parent company of American electric power which is headquartered in Charlotte, North Carolina is on the list of Most Admired Companies in the World in 2021 and the list of Best American Employer from Forbes. The company will report its first quarter 2021 results on May 10, before the market opens. In the last reported quarter, the company delivered a revenue shock of 0.98%, exceeding Zacks’ consensus forecast in 3 of the last 4 quarters and missing in 1 quarter, the average earnings surprise being 0.88%.

During the first quarter, the company’s service area experienced weather patterns that ranged from very dry conditions to cooler than normal temperatures and moderate rainfall. Thus, the overall weather pattern is expected to have a neutral impact on the up-line performance of quarterly utilities. “With DukeEnergy in Zacks Rating #3 (hold) and ESP in positive territory, investors may want to consider this stock after the earnings report. Recent revisions to earnings estimates suggest that good things are ahead for Duke Energy and this year’s earnings report will provide a clearer picture of whether the stock is worth considering a buyout.”

The Zacks Consensus Estimate for Q121 revenue is pegged at $6.21 billion, indicating a 4.4% increase from last year’s quarterly reported figure and for corporate earnings pegged at $1.24 / share, indicating an 8.8% increase from the quarterly reported figure. last year.

Customer growth and infrastructure investment across franchises are expected to increase revenue in Q121. From a cost perspective, Duke Energy’s impressive cost mitigation initiatives are expected to positively impact and the dynamic growth of the franchise service area and positive returns from investing in integrity management for the LDC gas business are also expected to make a strong contribution to bottom-line performance. Despite the recent cold and stormy weather, operating costs have increased in certain areas.