Pound sterling gains ground while banking fears overshadow spring statementBoE to mull risks of hiking in the midst of a potential banking crisis, UK CPI and FOMC up first. Summary of economic projections due too

Pound sterling, despite the positive forecasts, is yet to really show a significant change in the fundamental data apart from PMI data. Inflation remains in double digits, GDP growth for Q4 revealed a contraction after the smallest of expansions in Q3 (0.1%). The bearish outlook for this forecast takes into account the incredibly challenging task of the Bank of England (BoE) to hike rates while banking stocks attempt to fight off a wave of selling as fears of systemic risk rippled through global banks after the collapse of three midsized US banks.

Pound Sterling had a rather strong week on the face of it. Cable rallied into the end of the week to close the week higher, EUR/GBP declined and GBP/CHF headed into the weekend around 2% higher for the week.

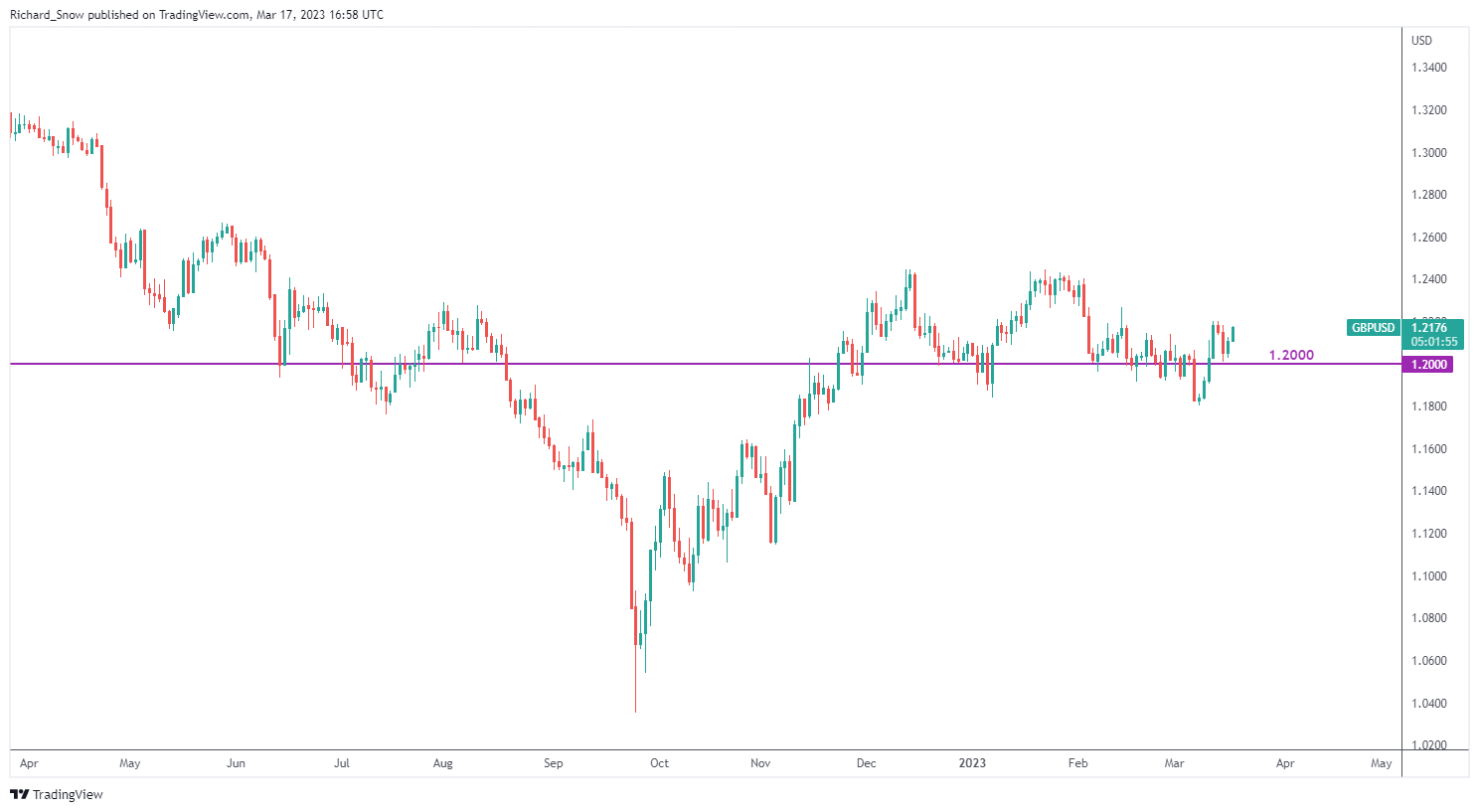

GBP/USD Daily Chart

Source: TradingView, prepared by Richard Snow

Jeremy Hunt’s Spring Statement started very strongly as the chancellor communicated the Office for Budget Responsibility’s (OBR) forecast that anticipates that the UK will avoid a technical recession and that inflation will more than halve, from 10.7% in November to 2.9% by the end of 2023. A minor contraction of 0.2% is now expected, a massive improvement from the prior November figure.

The budget statement involved a 3-month extension of the $2500 energy price guarantee, raised corporate taxes to 25%, abolished the lifetime allowance on pensions savings entirely, and introduced economic incentives to attract early retirees, the long-term sick and new parents back into employment among other measures.

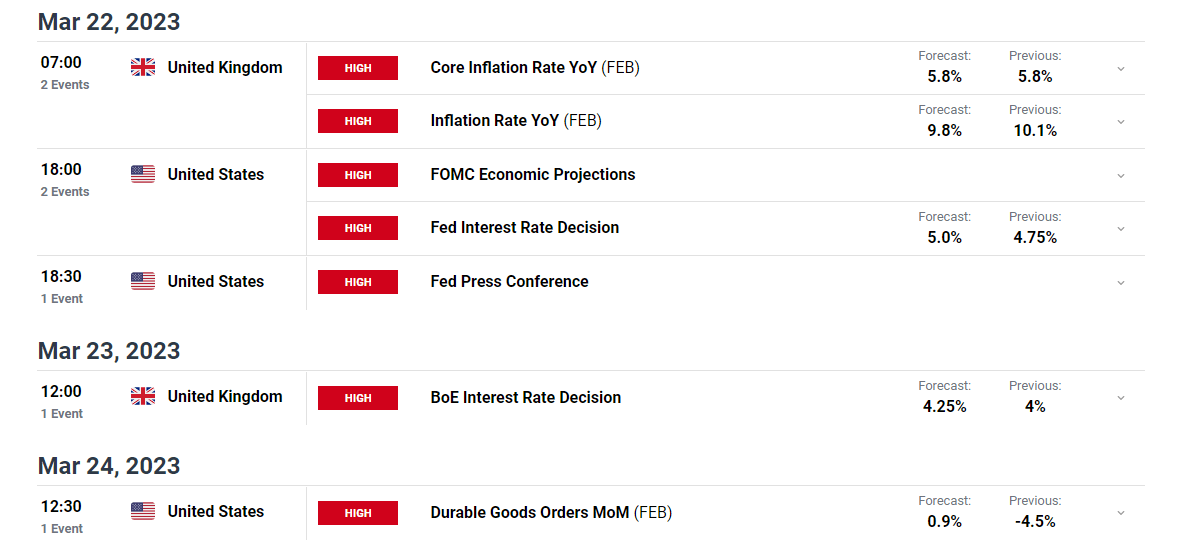

UK core inflation is forecast to remain sticky, with no year-on-year change for the month of February. Headline inflation is anticipated to dip into single digits, with prices expected to have risen 9.8% compared to February last year. Core inflation (inflation excluding volatile food and fuel prices) is a better gauge of wide-spread price pressures particularly when energy prices have declined drastically.

The BoE will certainly monitor the data print with great interest before deciding whether to hike by 25 basis points or take a more cautious approach given the massive volatility that has ensued after global banking fears.

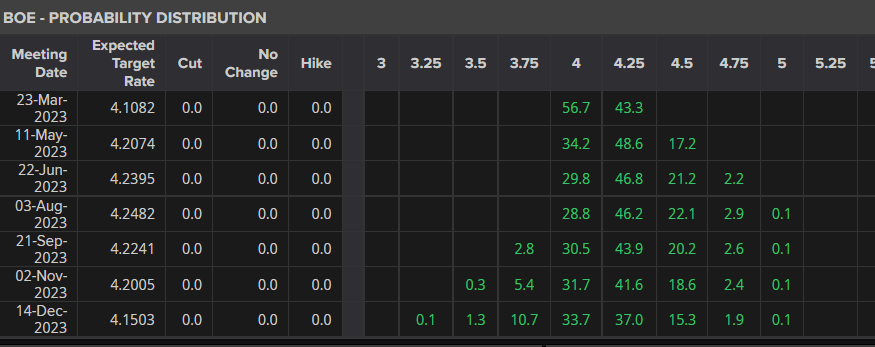

Current implied probabilities suggest an almost 50/50 split between no change in interest rates and a 25-basis point hike. Either way, sterling has shown a reluctance to strengthen in the wake of prior hikes as this simply exacerbates the cost-of-living crisis, while a decision not to hike could see sterling trade lower into the end of the week.

BoE Implied Rate Hike Odds

Source: Refinitiv, prepared by Richard Snow

The FOMC has been at the forefront of rate hikes which has helped bring about a disinflationary trend in the general level of prices. With progress being made on taming inflation, perhaps the Fed has more room than the ECB and BoE to consider no change to the Fed funds rate. Although, the committee will be well aware of how hot the US economy is operating – posing upside risks to inflation. Again, it’s a very tough call, although the added liquidity measure announced by the Fed for banks who require it, may provide the FOMC with the confidence needed to hike 25 basis points.

Customize and filter live economic data via our DailyFX economic calendar

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

{kind=link}

{kind=link}

{kind=link}