After a blistering Q1 for the Financial sector, a rockier road might await as they begin reporting their latest numbers this week. Expectations for Q2 results are down a bit after some of the banks warned of a slowdown in trading revenue.

While year-over-year earnings are expected to rise sharply for companies like

Bank of America (NYSE: BAC), Citigroup (NYSE: C), and Morgan Stanley (NYSE: MS), any drop in trading could weigh on year-over-year revenue growth. Remember that a year ago, trading was frantic during the pandemic, and it’s calmed down quite a bit over the last few months. That probably means fewer people making trades in both fixed income and equities, where some of the biggest banks harvest a lot of their cash.

Also, credit cards got a workout in Q1 as the economic recovery generated consumer demand. While shoppers remain in good shape judging from recent strong consumer confidence data, savings rates have spiked thanks in part to government checks. Many payment processing companies report that customers have been paying off balances. That’s not so good for bank revenue, either, considering high balances typically generate heavier interest payments.

Meanwhile, spending on big-ticket items like vehicles and housing is up, but those aren’t the kind of purchases people make by taking a card out of their wallet. Any drop in credit card activity can hurt consumer-focused firms like BAC and C.

With BAC, trading revenue continues to be under a microscope. The company scored big in that category last time out after missing Wall Street’s estimates in Q4.

C’s credit card business will get scrutiny to see how that’s holding up as consumers seem to be in a transitory mode. BAC and C both are straight ahead Wednesday, and MS, the last of the big banks to report this week, is expected to open its books on Thursday.

Net Interest Income Woes Could Plague Banks

For all the banks, pressure may come on the net-interest income side of the equation with Treasury yields falling throughout Q2. However, banks have shown the ability to make money even when those margins get squeezed, as we’ve seen often in recent years.

Remember that despite banks having mostly unveiled strong Q1 earnings, their stocks didn’t really ride the wave. It wouldn’t be surprising to see the same thing happen this time around, even if results exceed expectations, because many analysts expect the second half of 2021 to be tougher due to slowing economic growth. You could argue a lot of good news is already built into bank stocks.

Heading into earnings season, FactSet projects overall S&P 500 Financial Sector (IXM) earnings to rise an amazing 117% year-over-year in Q2, so things are definitely looking up on the bottom line. Keep in mind, however, that it’s a low bar.

Last year’s Q2 earnings for the industry were compressed in part by many big banks putting money aside for reserve in case of Covid-related defaults. A lot of that money is now being taken out of the reserve, which could create an impression of organic profit growth where none actually exists. As always, remember that bottom-line numbers aren’t always the best way to judge exactly how healthy a company might be.

To see how that works, look no further than average analyst estimates for Q2 Financial revenue. The average projection is for growth of just 4.4% year-over-year, according to FactSet. That’s the lowest of any sector and compares with expectations for nearly 20% growth in overall S&P 500 earnings. It’s also a slowdown from 9.5% revenue growth in Q1 for Financials.

Because the numbers are so bifurcated, it might be especially important for investors to pay attention to what the bank executives say about the near future in their earnings calls. Will merger and acquisitions (M&A) activity pick up in Q3? How’s the initial public offering (IPO) picture? Can the industry roll with the punches from falling yields and slower trading activity? Its ability to do that could have a major impact on stocks overall because Financials are often a leading sector.

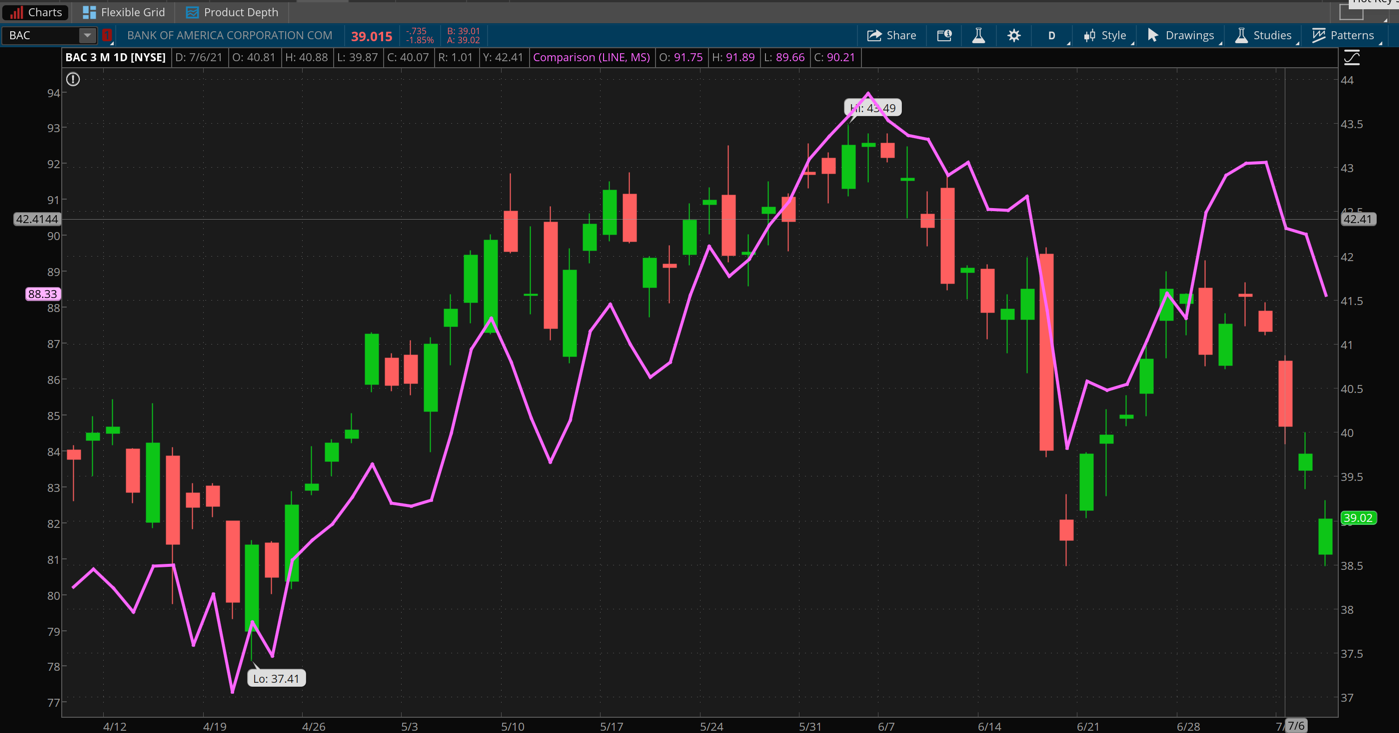

FIGURE 1: UPS AND DOWNS. After a very strong start to Q2, shares of both Bank of America (BAC—candlestick) and Morgan Stanley (MS—purple line) ran into trouble late in the quarter and again early this month as Treasury yields fell. Data source: NYSE. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Bank Of America Seen As A Consumer Barometer

Consumer confidence continued to be strong in the latest report from the Conference Board, which could be a positive development for BAC, which derives the highest amount of its revenue from consumer banking.

Like other banks, though, BAC could face challenges from the rate side of the equation. You can’t fight the Fed, and banks certainly can’t. The continued near-zero interest rate policy of the central bank kept 10-year Treasury yields under pressure much of Q2, which could hurt BAC’s net interest income.

BAC, like banks in general, makes money by borrowing at a low rate and lending at higher rates. A narrowing yield curve—where longer-term yields have been falling more quickly than the short-term ones—tends to weigh against BAC and other banks.

The 2/10 yield curve—or the gap between the two-year and 10-year yields—recently fell to around 108 basis points, down from approximately 150 basis points earlier this year. BAC, which in Q1 earnings warned investors that low-interest rates remained a revenue “challenge” saw more of that in Q2.

BAC is often thought of as the big bank most exposed to interest rates due to its large base of deposits, so it probably has more to gain (or lose) than some of its rivals based on where rates go.

One thing that may have worked in BAC’s favor earlier in Q2 was a hot housing market. Housing prices continued their long rise, which could mean bigger revenue for BAC’s mortgage business even though mortgage rates remained relatively low.

In one positive development for banks like BAC with big consumer divisions, the sizzling housing market and continued strength in U.S. manufacturing mean more households and businesses might have been out there borrowing last quarter.

On a less bullish note, mortgage applications recently dropped to pre-pandemic levels and refinancing of mortgages has dropped several months in a row. Rising home prices and insufficient supplies seem to have gummed up the housing market a bit.

Costs are another thing to watch when BAC reports. Shares of BAC fell after it reported Q1 earnings, and some analysts blamed rising costs. Weaker than expected loan growth that quarter might also have weighed, so check and see if that improved in Q2.

Credit Check At Citigroup

Like BAC, Citigroup has often been considered a good consumer barometer thanks to its huge credit card business. If consumers were happier in Q2, and they seemed to be, that could be a driving factor in C’s potential earnings success.

With C, it also helps to understand what’s going on in Europe, because its loan book is heavily exposed to that economy. Though the euro has been coming down vs. the dollar lately, it was strong through much of Q2, which may be a helpful sign of solid growth overseas that could play into C’s hands.

The U.S. 10-year Treasury yield recently traded at a 160-basis point premium to the benchmark 10-year German bund yield, down from 190 points at the end of Q1. This might also be a helpful development for C, at least if you’re looking at its business in Europe.

One problem for C and some other banks in Q2 might have been the relative scarcity of special purpose acquisition companies (SPACs), a field where C is one of the dominant players. SPACs exploded late last year and early in 2021, but then leveled out in Q2. This could hurt C’s investment banking business, which was explosive in Q1.

Last time out, C beat the Street’s expectations, but part of its profit improvement came from releasing some reserves it had put aside in case of possible Covid-related loan losses. C said it had released $3.9 billion in loan-loss reserves during Q1. Generally, analysts don’t view releasing these reserves as organic profit growth. Some of that could continue in Q2 for C and other banks as the Covid retreated in the U.S. thanks to vaccines.

The company’s earnings call could be a chance for investors to get an update on what CEO Jane Fraser calls a “refresh of our strategy” that includes shifting some of its non-U.S. consumer banking operations.

Morgan Stanley

Last time out, Morgan Stanley easily beat analysts’ revenue and earnings estimates thanks in part to booming capital markets that helped spark business in SPACs and wealth management. Since then, both of those factors have been put on simmer, raising questions about how MS can follow up in Q2.

You may think of MS mainly in terms of capital markets and wealth management, but remember the bank is trying to get a bite of the retail market with recent acquisitions. The company’s earnings call offers investors a possible chance to get updates on how that’s going. Unfortunately for MS, it’s unclear if retail trading in Q2 could have kept up with the pace we saw back in Q1 and during the pandemic. The so-called “meme” stocks that helped drive Q1 trading interest definitely died down a bit in Q2.

One thing to consider: MS is usually the last of the “significant six” big banks reporting, meaning investors may have its performance under a microscope to see if it did as well as other banks closely linked to the capital markets like JPM and GS.

As always, it’s important to keep an eye on MS’s investment banking revenue, which reached $2.61 billion in Q1, exceeding Wall Street analysts’ expectations by around $500 million. Wealth Management is another huge division for MS and jumped 47% to $5.96 billion in Q1. That could be hard to match.

In Q1, MS reported returns on tangible common equity of 21.1%. It’s an important number to watch for clues into how the bank performed in Q2.

Bank of America Earnings And Options Activity

Bank of America is expected to report adjusted EPS of $0.77 vs. $0.37 in the prior-year quarter, on revenue of $21.59 billion, according to third-party consensus analyst estimates.

Options traders have priced in a 2.9% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator on the thinkorswim® platform. Implied volatility is at the 20th percentile as of Tuesday morning.

Looking at the July 16 expiration, put options have concentrations at the 39 and 40 strikes. Calls have been active at the 42 and 43 strikes.

Citigroup Earnings And Options Activity

Citigroup is expected to report adjusted earnings of $1.98, vs. $0.5 in the prior-year quarter, on revenue of $17.29 billion, according to third-party consensus analyst estimates. Revenue is expected to be down 9.6% year-over-year.

Options traders have priced in a 2.4% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. Implied volatility was at the 14th percentile as of Tuesday morning.

Looking at the July 16 options expiration, put volume has been light overall, but with some activity at the 65 strike. Calls have seen more activity, particularly at the 70 and 75 strikes.

Morgan Stanley Earnings And Options Activity

Morgan Stanley is expected to report adjusted earnings of $1.64, vs. $1.01 in the prior-year quarter, on revenue of $13.96 billion, according to third-party consensus analyst estimates. Revenue is expected to be up 47.3% year-over-year.

Options traders have priced in a 2.5% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. Implied volatility was at the 17th percentile as of Tuesday morning.

Looking at the July 16 options expiration, the volume has been muted to the downside, with some activity at the 85- and 90-strike puts. Calls have seen more activity, with concentrations at the 95 and 100 strikes.

TD Ameritrade® commentary for educational purposes only. Member SIPC. Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options.

The preceding article is from one of our external contributors.

It does not represent the opinion of Benzinga and has not been edited.

© 2021 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.